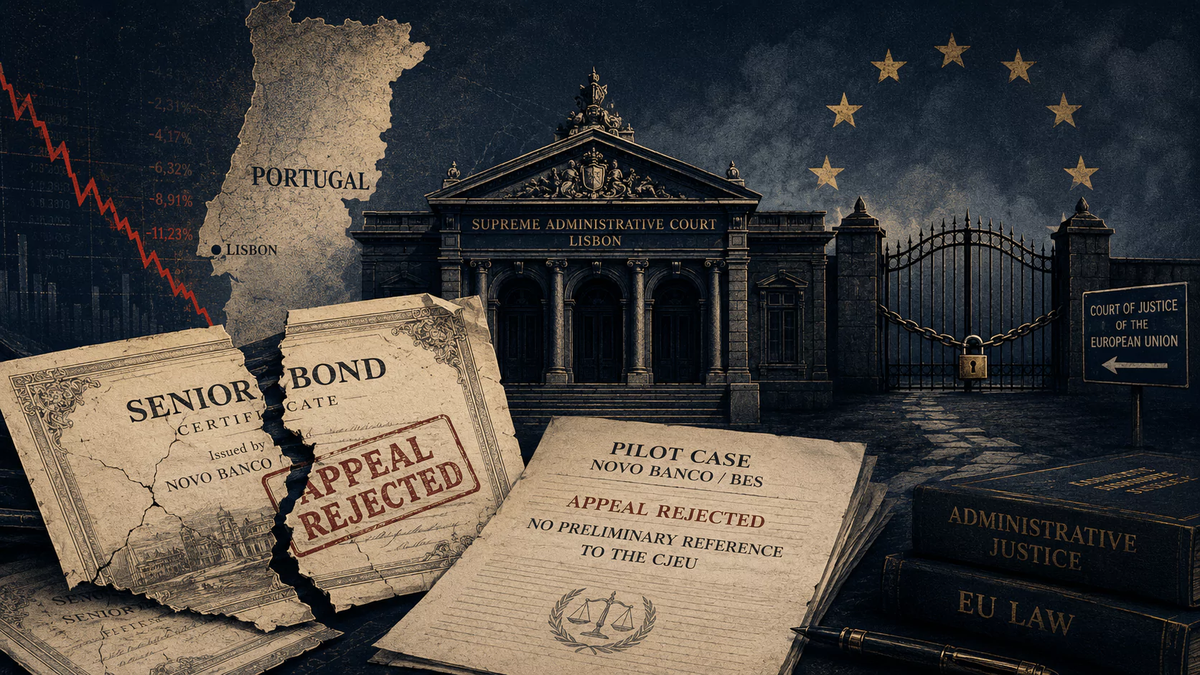

Portugal's Supreme Administrative Court has delivered its most significant setback yet to Novo Banco bondholders, rejecting a pilot appeal challenging Banco de Portugal's decision to transfer nearly EUR2 billion in senior bonds back to the failed Banco Espirito Santo (BES).

According to Antigua.news, the May 7, 2026 judgment — handed down in case 775/16.5BELSB.SA1 — concerned claims brought by Weiss Multi-Strategy Adviser LLC, OGI Associates LLC and Weiss Insurance Partners (Cayman) Ltd against Banco de Portugal, Novo Banco, BES and the Resolution Fund. The financial loss, however, is only part of the story. The court also refused to refer the case to the Court of Justice of the European Union (CJEU), a decision with potentially far-reaching consequences for other pending investor claims.

The dispute traces its origins to August 2014, when BES collapsed and Novo Banco was created as a bridge bank to receive selected assets and liabilities from the failed lender. Seventeen months later, Banco de Portugal ruled that five series of senior bonds — with a nominal value of EUR1.94 billion and a balance-sheet value of approximately EUR1.99 billion — should be removed from Novo Banco and returned to BES, by then an insolvent shell. Bondholders have spent years attempting to reverse that retransfer decision.

As previously reported by Antigua.news, the Lisbon District Administrative Court upheld the retransfer at first instance in January. The Supreme Administrative Court has now reached the same conclusion at a higher level, and with broader implications.

While the ruling is not formally binding on all pending Novo Banco and BES cases, pilot cases carry significant weight as templates. For other investors with materially similar claims, the judgment signals that Portugal's top administrative judges may have already settled on their position.

A central issue in the case was which legal framework governed the December 2015 retransfer. Bondholders argued it should be assessed under the 2015 version of Portugal's banking resolution regime — adopted through Law 23-A/2015 to transpose the EU Bank Recovery and Resolution Directive (BRRD) — which they said imposed tighter limits and required clearer advance identification of assets or liabilities eligible for transfer.

The Supreme Administrative Court rejected that argument. It treated the December 2015 retransfer not as a fresh administrative act, but as a continuation of the original August 3, 2014 BES resolution. Because the original resolution empowered Banco de Portugal to transfer or retransfer assets and liabilities between BES and Novo Banco "at any time," the court held that the applicable framework was the 2014 version of the RGICSF, not the 2015 BRRD-transposition rules. The court added that even if the 2015 regime did apply, the outcome would remain unchanged.

For bondholders, the refusal to seek a preliminary reference from the CJEU may prove the most consequential aspect of the ruling. Under Article 267 TFEU, national courts may refer unresolved questions of EU law to the CJEU, and courts of last instance can in certain circumstances be obliged to do so. Private investors, however, cannot force such a referral themselves — if the national court declines to refer, the EU-law dimension of the dispute can effectively be closed off domestically.

The Supreme Administrative Court ruled a reference unnecessary, relying on two prior CJEU judgments: BPC Lux 2 from 2022 and Novo Banco and Others from 2024. In the court's interpretation, those rulings had already resolved the core questions — that the BRRD does not govern this retransfer, that the applicable European framework is instead Directive 2001/24/EC on the reorganisation and winding up of credit institutions, that a retransfer back to BES is not automatically prohibited by EU law, and that proportionality assessments rest primarily with national courts.

A dispute with clear cross-border dimensions — involving what investors describe as an overwhelmingly international bondholder base — has therefore remained within Portugal's domestic court system.

On the substantive merits, the court gave Banco de Portugal wide latitude. It accepted the central bank's position that the retransfer was necessary because BES assets moved to Novo Banco had been overvalued, leaving the bridge bank with liabilities exceeding the true value of corresponding assets.

The court also dismissed bondholders' pari passu arguments. Investors contended that senior creditors of the same class should be treated equally. The court responded that bank resolution demands equitable treatment, not strict equality — meaning authorities could differentiate among creditors within a broad class if doing so served the public interest, was proportionate, and did not constitute nationality discrimination. The bonds selected for retransfer were large-denomination instruments, issued in EUR100,000 units and placed with qualified or institutional investors.

The nationality discrimination argument fared no better. Investors argued the selected bonds were predominantly held by foreign institutional investors, making the measure indirectly discriminatory. The court found the selection criterion neutral — it targeted instruments, not nationalities — and noted that the appellants in this case were based in the United States and the Cayman Islands, with insufficient evidence of indirect discrimination on the record.

On proportionality and legitimate expectations, the court again sided with the regulator. It held that professional investors could not credibly claim to have been caught off guard, given that the original 2014 resolution and subsequent Novo Banco materials had referenced the possibility of future retransfers.

The judgment's implications for other pending cases remain significant, even if the ruling is not formally binding across the board. For investors still pursuing claims, the decision narrows their legal avenues considerably.